Millions of UK pensioners are now discovering a surprising truth about retirement finances: two people with almost identical incomes can end up paying completely different amounts of tax depending on how their pensions and savings are structured.

Financial experts warn that many pensioners may unknowingly lose hundreds — or even thousands — of pounds each year because of small differences in:

- Pension withdrawals

- Tax codes

- Savings interest

- Private pension timing

- Income structure

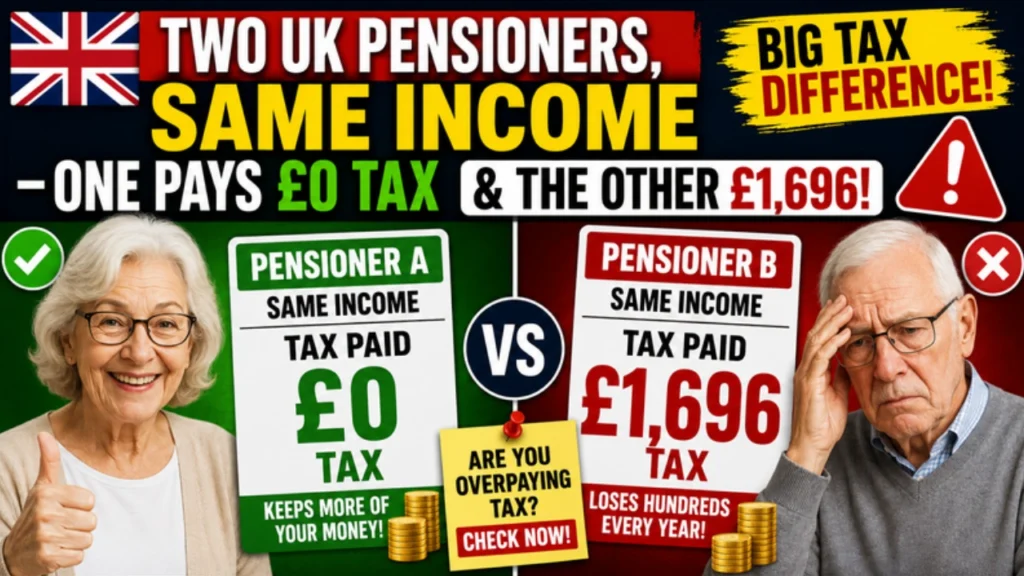

In some cases, one retiree could legally pay almost no income tax while another with a similar retirement income faces a tax bill worth more than £1,600 annually.

Why Pensioners Are Suddenly Paying More Tax

One of the biggest reasons is something economists call “fiscal drag.”

Although pension income and State Pension payments continue rising, the UK personal tax allowance remains frozen at:

- £12,570

This means more retirees are slowly being pulled into paying income tax each year even without becoming significantly wealthier.

How Two Pensioners Can Pay Completely Different Tax

Experts say retirement taxation depends heavily on how income is received.

For example:

- One pensioner may rely mainly on ISA savings and structured withdrawals

- Another may take larger taxable private pension payments

Even if total income appears similar, the tax outcome can change dramatically.

Common factors affecting pension tax include:

- Private pension withdrawals

- State Pension amounts

- Savings interest

- Employment income

- Emergency tax codes

- Marriage Allowance eligibility

Emergency Tax Is Catching Thousands of Retirees

One major problem involves pension withdrawals triggering emergency tax systems.

Some retirees withdraw large lump sums without realising HMRC may temporarily assume:

- The same amount will continue every month

ISAs Are Becoming More Important for Pensioners

Financial advisers increasingly recommend tax-efficient retirement planning using:

- Cash ISAs

- Stocks and Shares ISAs

- Structured withdrawals

because ISA income is generally protected from UK income tax.

Meanwhile, private pension withdrawals may still count toward taxable income limits.

Marriage Allowance Could Also Reduce Tax Bills

Thousands of older couples may legally reduce tax through Marriage Allowance but never claim it.

Eligible spouses may transfer part of their unused tax-free allowance to a partner, potentially lowering overall household taxation.

Experts say many retirees are simply unaware the scheme exists.

Pensioners Are Also Being Hit by Savings Interest Tax

Higher UK interest rates have created another unexpected problem.

Many retirees now earn larger amounts of interest from:

- Savings accounts

- Fixed deposits

- Cash investments

However, some pensioners unknowingly cross taxable interest thresholds.

Experts Warn Pensioners To Check Their HMRC Tax Code

One of the most common retirement mistakes involves incorrect tax coding.

Errors may happen when:

- State Pension begins

- Multiple pensions exist

- Employment ends

- Pension providers submit outdated information

An incorrect code may cause overpayments lasting months or even years.

What Pensioners Should Do Right Now

Financial experts recommend retirees:

- Review tax codes carefully

- Monitor pension withdrawals strategically

- Check ISA usage

- Review savings interest levels

- Explore Marriage Allowance eligibility

Pensioners concerned about taxation are also encouraged to seek independent financial guidance when necessary.

Could Pension Taxes Rise Further?

Analysts believe pension taxation debates may intensify further because:

- Britain’s ageing population is growing

- State Pension spending continues rising

- Public finances remain under pressure

Some economists believe future governments may eventually face difficult decisions involving:

- Tax thresholds

- Pension relief

- Retirement allowances

- Savings taxation

Conclusion

The growing difference in how UK pensioners are taxed is creating major concern as millions of retirees discover that small financial decisions can dramatically affect retirement income. While some pensioners legally pay little or no income tax, others with very similar incomes may lose thousands due to tax structure differences, emergency deductions, or frozen thresholds.